It is still August and the CFPB already has been active this year with significant new final and proposed rules, advisory opinions, supervision findings, enforcement proceedings, and circulars (detailed interpretations) covering a wide range of new and established financial products. This activity often can be of significant benefit to consumers litigating in these areas and can help their attorneys identify systematic abuses in various industries. This article briefly summarizes 18 such CFPB actions and their implications for private consumer litigation.

Land Installment Sale Contracts (Contracts for Deed) Must Comply with TILA

An August 13, 2024, the CFPB issued an advisory opinion, Truth in Lending (Regulation Z); Consumer Protections for Home Sales Financed Under Contracts for Deed, that affirms the applicability of the Truth in Lending Act (TILA) and its Regulation Z to transactions in which a consumer purchases a home under a “contract for deed,” including TILA’s protections associated with residential mortgage loans. The opinion will be effective as soon as published in the Federal Register.

Contracts for deed are extensively utilized today and lead to significant consumer abuses. Clarifying TILA’s application should strengthen consumer challenges to these transactions where the homebuyer makes periodic payments, often from 5 to 30 years, while the seller retains the deed. Homes typically are purchased without appraisals at inflated prices and sold “as is” with significant condition issues. The buyer pays for taxes, insurance, maintenance, and repairs, but, if the borrower defaults, the buyer generally forfeits their entire investment—including their down payment, principal payments, and any increase in home equity. These contracts are examined extensively, including applicable federal and state laws, in NCLC’s Mortgage Lending Chapter 11.

The advisory opinion provides a detailed analysis explaining why TILA applies to these transactions. It discusses important protections that flow from TILA, including the requirement that a creditor make a reasonable, good faith determination of the consumer’s ability to repay, additional protections for high-cost loans under HOEPA, and TILA’s prohibition on mandatory arbitration clauses in home mortgage loans. These transactions may also be subject to TILA and RESPA mortgage servicing rules regarding periodic statements, escrow accounting, and loss mitigation if the transaction is a federally related mortgage under RESPA. See NCLC’s Mortgage Servicing and Loan Modifications § 3.2.1.

Buy Now, Pay Later Loans to Purchase Goods Now Covered By TILA

A CFPB interpretive rule, 89 Fed. Reg. 47,068 (May 31, 2024), explains why buy now, pay later (BNPL) accounts are a form of credit card under the Truth in Lending Act (TILA), so that BNPL accounts must comply with certain TILA credit card provisions. BNPL credit is a fast-growing form of lending that enables consumers to split the cost of purchases into four or more payments. The most common BNPL credit involves “pay-in-four” purchases, where consumers pay 25% of the cost of the item at the point of sale, and the remaining balance in 3 payments of 25% over the next 6 weeks. Once they establish a BNPL account, consumers can use that account repeatedly to make additional purchases, just as they can with a credit card.

Consumers often get the runaround between the merchant and the lender when they are unhappy with a purchase and can find themselves on the hook for payments when filing disputes, which can take weeks to resolve. Consumers can also easily lose track of when payments are due, particularly if they have multiple outstanding BNPL loans.

The CFPB is now ruling that BNPL lenders must, as of July 30, 2024, comply with the credit card requirements under Part B of Regulation Z, and thus should be subject to TILA private remedies. BNPL lenders must:

- Investigate consumer disputes and pause payment requirements during the investigation and issue credits as applicable.

- Credit the refunds to consumers’ accounts when consumers return products or cancel services for a refund.

- Send consumers periodic billing statements.

CFPB Explains Why Earned Wage Advances Must Comply with TILA—Even Though Many Don’t Now

In July, the CFPB issued a proposed interpretative rule to address evasions by fintech payday lenders that hide the cost of 300% annual percentage rate (APR) loans and evade state rate caps. See 89 Fed. Reg. 61,358 (July 31, 2024). The proposal intends to overturn a 2020 advisory opinion that found certain wage advances not covered by TILA, and the 2024 proposal instead rules that paycheck advances are loans that must comply with TILA and that most so-called “tips” and other junk fees are finance charges under TILA.

While the CFPB action at this point is only a proposal, the Federal Register notice provides a compelling analysis why earned wage advances are in fact covered by TILA. TILA requires APR disclosures if the finance charge exceeds $5, or $7.50 for loans of $75 or higher. The CFPB’s analysis should be strong support for any private litigation against earned wage advances that violate TILA. See also NCLC’s Truth in Lending § 2.8.10; NCLC’s Consumer Credit Regulation § 9.10.

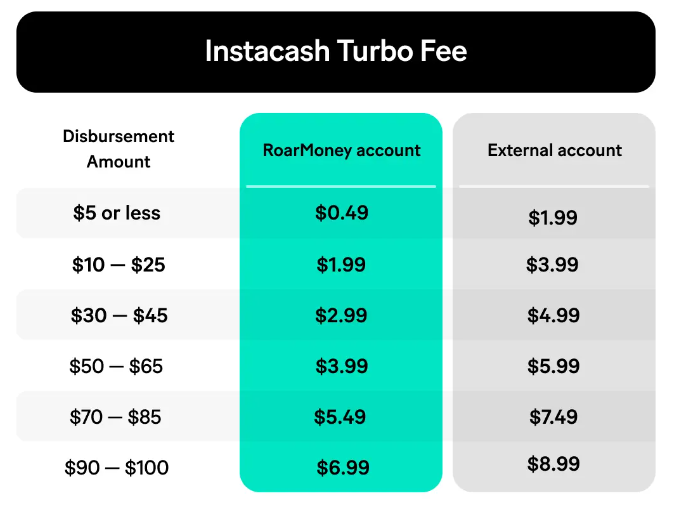

Earned wage advances involve some of the most abusive loans today. EarnIn disclosed 0% APR for a $100 loan but inserted a so-called tip of $11; with a $4 expedite fee included, the true APR would be 498%. California’s regulator found that 73% of transactions that solicited tips included them and identified “multiple strategies that lenders use to make tips almost as certain as required fees.” The cost of sending loans instantly is generally about 4.5 cents or lower, but MoneyLion charges an inflated “turbo fee,” which increases as the loan increases, up to $8.99 for an advance of $100, while claiming “no interest.”

The CFPB released data from several lenders that offer paycheck advances through employers, finding that the average worker is stuck in a cycle of reborrowing, taking out 27 loans a year (and some over 40) with an average APR over 100%, but potentially as high as 580.4%. While some employers offer early pay for free, the CFPB found that over 90% of workers paid one or more fees, primarily expedite fees, and that speed was an “integral feature” of the credit.

California data on both employer-based and direct-to-consumer loans found average APRs for both types over 330% and an average of 36 loans a year. Other research shows that cash advance apps lead to an increase in overdraft fees, just like other payday loans.

Registry of Enforcement Actions Against Non-Banks

The CFPB on June 3 finalized a rule, effective September 16, 2024, that establishes a registry to detect and deter corporate offenders that have broken consumer laws and are subject to federal, state, or local government or court orders since January 1, 2017. Non-bank companies must register with the CFPB when they have been caught violating consumer law, including certain final agency and court orders and judgments, also including consent and stipulated orders brought under consumer protection laws. The companies must also provide a written attestation from an executive that confirms compliance with any relevant orders.

Registration will begin for covered nonbanks as early as October 16, 2024. The deadline for Larger Participant, CFPB-Supervised Covered Nonbanks is January 14, 2025. The deadline for other CFPB-Supervised Covered Nonbanks is April 14, 2025. The deadline for all other covered banks is July 14, 2025.

The registry will be used by state attorneys general, state regulators, and a range of other law enforcement agencies. The registry will also assist investors, creditors, business partners, and members of the public that are conducting due diligence or research on financial firms bound by law enforcement orders. And, of course, the registry may prove helpful for consumer litigation against businesses found in the registry that continue to violate the law.

CFPB Examination Finds Numerous Mortgage Servicing Violations

The CFPB’s Supervisory Highlights: Mortgage Servicing Edition Issue # 33 (Spring 2024) focuses on unfair and deceptive mortgage servicing practices (which thus may be state UDAP violations) and other practices that violate RESPA Reg. X or TILA Reg. Z. The following list may prove helpful for practitioners representing homeowners, suggesting areas of abuse:

- Mortgage servicers charged homeowners for property inspections following the homeowner’s delinquency on Fannie Mae loans where such inspections were prohibited by Fannie Mae guidelines.

- Mortgage servicers assessing late fees that exceeded the amount allowed in the loan agreement or even where consumers entered into loss mitigation agreements and RESPA Reg. X prohibits such late fees.

- Mortgage servicers offered streamlined COVID-19 loan modifications but, in violation of Reg. X, failed to waive existing fees after borrowers accepted the modifications.

- Mortgage servicers failed in billing statements to provide a brief description of certain fees and charges in violation of TILA Reg. Z when they used the general label “service fee” for 18 different fee types, without including any additional descriptive information.

- Servicers violated Reg. X when their first attempt to make escrow disbursements did not reach the payees, the servicers did not resend the payments until months after the initial payment attempts.

- Servicers sent notices that consumers had been approved for a streamlined loss mitigation option even though the servicers had not yet determined whether the consumers were eligible for the option and some consumers were ultimately denied the option.

- Servicers sent notices informing consumers that they had missed payments and should fill out loss mitigation applications when the consumers were current on their payments, in a trial modification plan, or the loan was paid off or subject to short sale.

- Servicers violated Regulation X by sending acknowledgment notices to borrowers that failed to specify whether the borrowers’ applications were complete or incomplete, did not provide timely notices stating the servicers’ determination regarding loss mitigation options, or did not provide a deadline for accepting or rejecting loss mitigation offers.

- Servicers did not follow investor guidelines for evaluating loss mitigation applications when they automatically denied certain consumers a payment deferral option rather than submitting the consumers’ applications to the investor for review.

- Servicers violated Reg. X when they failed to make good faith efforts to establish live contact with delinquent borrowers.

- Servicers violated Reg. X when they failed to send written early intervention notices to delinquent borrowers

- Servicers violated Reg. X when they failed to document certain actions in their servicing systems, such as establishing live contact with borrowers.

For litigation advice involving these abuses, see NCLC’s Mortgage Servicing and Loan Modifications.

CFPB Explains Why Credit Reporting Practices Violate the Fair Credit Reporting Act

A January CFPB advisory opinion addresses accuracy issues in background check reports, which most employers and landlords use to screen workers and renters under the Fair Credit Reporting Act (FCRA). The advisory opinion affirms that, when preparing consumer reports, a consumer reporting agency (CRA) that reports public record information—including employment and tenant screening companies—is not using reasonable procedures to assure maximum possible accuracy under FCRA § 1681e(b) if it does not have procedures in place to prevent reporting of duplicate information and expunged, sealed, or otherwise restricted information. The CRA must also report any existing disposition information if it reports arrests, criminal charges, eviction proceedings, or other court filings. See 89 Fed. Reg. 4171 (Jan. 23, 2024).

FCRA § 1681c(a) limits the reporting of most adverse information to 7 years (the exceptions are for bankruptcies and criminal convictions). The advisory opinion also discusses the running of the 7-year period before information is obsolete and no longer reportable. It makes clear that the occurrence of the adverse event starts the running of the reporting period and is not restarted by subsequent events, and a non-conviction disposition of a criminal charge cannot be reported beyond the 7-year period that begins to run at the time of the charge. In other words, a CRA may not use the disposition date of a criminal record as the trigger date for the statute of limitations.

Another January CFPB advisory opinion addresses FCRA requirements for CRA disclosure to consumers of the contents of their files. See 89 Fed. Reg. 4167 (Jan. 23, 2024). To trigger a CRA’s file disclosure requirement, a consumer need not use specific language, such as “complete file” or “file.” CRAs must disclose to a consumer both the original source and any intermediary or vendor source (or sources) that provide the item of information to the CRA. Additionally, the advisory opinion states that FCRA § 1681g(a)(1)’s requirement to disclose to the consumer “all information in the consumer’s file at the time of the request” means that, even when a user only received a score or summary, the CRA must disclose all information that formed the basis of the score or summary. Finally, the advisory opinion notes that FCRA § 1681g(a) requires a CRA to provide a consumer with a file disclosure that accurately reflects the information that the CRA provided or might provide to a user.

Both advisory opinions are examined in more detail in an NCLC article earlier this year. See Chi Chi Wu, Ariel Nelson, Two New CFPB Advisory Opinions Facilitate Private FCRA Litigation.

The CFPB’s Supervisory Highlights: Consumer Reporting Companies and Furnishers, Issue # 32 (Spring 2024) focuses on common CRA and furnisher FCRA violations. Some CRAs automatically declined to implement identity theft blocks despite adequate consumer requests. CFPB examiners also found some CRAs violated the FCRA Regulation V’s human trafficking requirements by failing to timely block or fail to block at all adverse information identified by the consumer as resulting from human trafficking.

Examiners found several large furnishers violated the FCRA duty to promptly update or correct information determined to be incomplete or inaccurate, including by continuing to report fraudulent accounts to CRAs as valid accounts for several years after determining the accounts were fraudulent. Some furnishers also failed to respond to identity theft reports.

For details on bringing FCRA litigation involving these abuses, see NCLC’s Fair Credit Reporting.

CFPB Finds Debt Collectors Flouting Regulation F

The CFPB’s Supervisory Highlights: Servicing and Collection of Consumer Debt, Issue #34 (Summer 2024) includes a focus on debt collector practices that violate the FDCPA, Regulation F, or were otherwise are unfair, deceptive or abusive. Debt collectors:

- Failed to provide the requisite validation information when the debt collector had received notice that its prior written disclosure was not delivered to the consumer, and the debt collector failed to provide validation information within five days of the initial communication via telephone.

- Failed to provide validation notices at all when collecting on student loan debt.

- Used a business name other than the true name of the debt collectors’ business, and failed to disclose their true company names in violation of the FDCPA.

- Failed to comply with the requirement that collectors disclose that the collectors are attempting to collect a debt and that any information obtained will be used for that purpose.

- Sent payment reminder emails to the consumer before 8 a.m. in the consumer’s time zone.

- Continued the conversation even after the consumer indicated that it was an inconvenient time or place to talk.

- Were verbally abusive towards the consumers.

- Placed over 100 telephone calls to the consumers after the consumers requested that the debt collectors stop contacting them.

- Communicated via text message or phone call at a specific telephone number that the consumers had requested the debt collectors not use.

- Failed to include the required disclosure that the communication was from a debt collector in electronic payment confirmations from service providers.

Consumer law practitioners can be on the lookout for these FDCPA violations when interviewing clients. Specifics on these FDCPA violations can be found in NCLC’s Fair Debt Collection.

The CFPB examiners also found that card issuers sold thousands of credit card debts to debt collectors misrepresenting the applicable state’s statute of limitations for credit card debt as ten years rather than five years, including some accounts on which the statute of limitations had already expired. As a result, one can expect debt collectors collecting on and suing on debts years later to do so on debts that are beyond the applicable limitations period.

Abuses Committed by Major Automobile Creditors

A CFPB consent order with Toyota Motor Credit states that the auto creditor:

- Made it unreasonably difficult for consumers to cancel unwanted add-ons, including when consumers complained that dealers had forced add-ons on consumers without their consent;

- Failed to ensure consumers received refunds of unearned guaranteed asset protection and credit life and accidental health premiums when they paid off their loans early or ended lease agreements early; and

- Failed to provide accurate refunds to consumers who canceled their vehicle service agreements.

The CFPB also found that Toyota Motor Credit violated the FCRA by:

- Failing to promptly correct reports sent to CRAs that an account was delinquent even though customers had already returned their vehicles; and

- Failing to maintain reasonable policies and procedures to ensure related payment information it sent to CRCs was accurate.

The CFPB’s Supervisory Highlights: Servicing and Collection of Consumer Debt, Issue #34 (Summer 2024) includes a focus on automobile loan servicing. Auto servicers offered preauthorized recurring electronic fund transfer enrollment for consumers to make automatic payments on their loans but did not debit consumers’ final payments when the payments were a different amount from their regular monthly payments. Servicers failed to adequately communicate to consumers that they must remit the final payment manually, despite being enrolled in autopay. Servicers then charged consumers late fees for failing to make the final payment on time.

Student Loan Servicing Abuses

The CFPB’s Supervisory Highlights: Servicing and Collection of Consumer Debt, Issue #34 (Summer 2024) includes a focus on student loan servicing. The CFPB found that consumers faced excessive hold times when contacting loan servicers, with an average wait time of 40 minutes over a 6-month period. As a result of these long hold times, almost half of consumers dropped their calls before speaking with an agent. During that time period, the servicers also significantly understaffed their call centers and disabled consumers’ access to their online account management portals, making it difficult for borrowers to make payments online and access their loan information. The report also highlighted other barriers to assistance, including problems with servicers’ interactive voice response systems, limiting consumers’ ability to pay or obtain assistance accessing benefits without speaking to an agent.

In addition, On May 31, 2024, the CFPB sued student loan servicer PHEAA, which does business as American Education Services, for illegally collecting on student loans that have been discharged in bankruptcy and sending false information about consumers to credit reporting companies.

Litigation against student loan servicers is examined at NCLC’s Student Loan Law § 18.3.

Financial Institution Improper Practices After Bank Accounts Frozen or Closed

The CFPB’s Supervisory Highlights: Servicing and Collection of Consumer Debt, Issue #34 (Summer 2024) includes a focus on banks. The CFPB found that some institutions failed to affirmatively notify consumers after blocking their accounts. In other instances, institutions provided notices but failed to provide clear guidance to consumers, such as directing them to write in by mail for more information without specifying the information the consumer needed to unfreeze their accounts.

Institutions sometimes exacerbated these practices by frustrating consumers’ ability to contact the institution. For example, certain institutions dropped or blocked most calls from numbers associated with the frozen accounts so that consumers could not connect with a customer service representative to ask questions or challenge the freezes. In other instances, institutions automatically forwarded calls from these numbers to a pre-recorded message that did not provide meaningful information about the consumer’s account.

The CFPB also issued an order against Chime Financial, Inc. (Chime) on May 7, 2024. Chime is a financial-technology company that designs and services consumer banking accounts for two separate FDIC-insured “partner banks.” The CFPB found Chime engaged in unfair practices when it failed to timely refund remaining balances to consumers whose checking and savings accounts were closed.

For more on account freezes and closings, see the newly released Seventh Edition of NCLC’s Consumer Banking and Payment Law §§ 2.6, 6.9.

Current Abuses Involving Remittance Transfers

CFPB Circular 2024-02 focuses on deceptive marketing concerning the speed or cost of remittance transfers (international money transfer services) that could violate a state UDAP statute even when the provider is otherwise in compliance with Regulation E’s provisions on remittance transfers. The CFPB considers it deceptive to market remittance transfers:

- As being delivered within a certain time frame, when transfers take longer to be available for recipients;

- As “no fee” or “free” when in fact the provider charges fees;

- As having promotional fees or exchange rates without sufficiently clarifying when an offer is temporary or limited.

For example, the CFPB has issued an order against Chime, Inc. doing business as Sendwave, alleging that it misrepresented the speed and cost of its remittance transfers through its mobile application. Sendwave also violated the Electronic Fund Transfer Act (EFTA) and Reg. E by: (1) wrongly requiring customers to waive their rights; (2) failing to provide required disclosures, including the date of fund availability and exchange rate; (3) failing to provide timely disclosures; and (4) failing to investigate errors properly and maintain required policies and procedures for error resolution.

For more on the EFTA and remittances, see the just released Seventh Edition of NCLC’s Consumer Banking and Payment Law § 9.2.

CFPB Supervision Points to Systematic Credit Card Abuses

The CFPB’s Supervisory Highlights: Servicing and Collection of Consumer Debt, Issue #34 (Summer 2024) includes a focus on abuses involving medical credit cards. Dentists, and other healthcare providers promoted, offered, and sold medical credit cards to consumers, including the specifics of deferred interest promotions. Other confusion related to whether monthly payments would be allocated to their promotional or nonpromotional balances. Consumers felt pressured by healthcare providers to open a credit card while receiving treatment. The CFPB expects card issuers to control such abuses. Private litigation might involve the healthcare providers or even the card issuers.

Credit Card Penalty Fees Final Rule Not Yet in Effect

The CFPB in March amended TILA Regulation Z to address late fees charged by card issuers that together with their affiliates have one million or more open credit card accounts. See 89 Fed. Reg. 19,128 (Mar. 15, 2024), to amend 12 C.F.R. § 1026.52(b)(ii). The amendment, if it goes into effect, will have the practical effect of dramatically reducing most credit card penalty fees to $8, although there will be no private right of action for violations.

The Chamber of Commerce and others have challenged the rule in a Texas federal court, and the rule is currently stayed. In the most recent decision, the Fifth Circuit vacated the district court’s order transferring the case to the federal court in the District of Columbia. See In re Chamber of Com. of United States of Am., 105 F.4th 297 (5th Cir. 2024).

Mere Inclusion of Illegal or Unenforceable Contract Terms Is Deceptive

The June CFPB Circular 2024-03 warns against unlawful or unenforceable terms and conditions in contracts for consumer financial products or services. Companies use this fine print tactic to try to trick consumers into believing they have given up certain legal rights or protections, and the CFPB considers such terms and conditions to be deceptive.

The CFPB provides examples of just some unenforceable or illegal terms found in consumer contracts:

- A general liability waiver, which purports to fully insulate companies from suits even though most states have laws that create hosts of exemptions to these waivers.

- The Military Lending Act generally prohibits terms in certain consumer credit contracts that require servicemembers and their dependents to waive the “right to legal recourse under any otherwise applicable provision of State or Federal law . . . .” 32 C.F.R. § 232.8(b), implementing 10 U.S.C. § 987(e)(2).

- Mortgage rules implementing TILA prohibit terms that force homeowners into arbitration or other nonjudicial procedures to resolve problems with a mortgage transaction.

- General waiver provisions in home equity lines of credit provide that the borrowers waive all other notices or demands in connection with the delivery, acceptance, performance, default or enforcement of the agreement.

- Bank deposit agreements waive consumers’ right to hold the bank liable for improperly responding to garnishment orders when, in fact, this right could not be waived.

- Remittance transfer agreements and other bank agreements limit consumers’ error resolution rights, despite the Electronic Fund Transfer Act (EFTA) prohibiting “waiver of any right conferred” by the EFTA or any “cause of action” under EFTA. See 15 U.S.C. § 1693l.

- Auto loans that indicate that consumers cannot exercise bankruptcy rights, when in fact, waivers of bankruptcy rights generally are void as a matter of public policy.

- Clauses limiting consumer rights to post honest online reviews, since the Consumer Review Fairness Act of 2016 generally prohibits such clauses. See CFPB, Bulletin 2022-05: Unfair and Deceptive Acts or Practices That Impede Consumer Reviews (Mar. 22, 2022).

- College tuition payment plans that include forced arbitration provisions, waivers of the borrowers’ right to seek discharge and retain their own legal counsel, and misrepresentations of borrowers’ legal right to discharge private student loans in bankruptcy. See CFPB Report Finds College Tuition Payment Plans Can Put Student Borrowers at Risk (Sept. 14, 2023).

- Arbitration or other provisions that limit class actions in court for violations of the Servicemembers Civil Relief Act. See CFPB, Ensuring Servicemembers Can Protect Themselves from Unlawful Financial Practices (Apr. 11, 2024).

- Waiver of a consumer’s state law right to block creditors from seizing the consumer’s property in which they do not hold security interests. See FTC Credit Practices Rule, 16 C.F.R. § 444.2(a)(2).

- Waivers that are inconsistent with numerous state laws that prohibit or restrict the use of waivers in consumer contracts.

The problem with private litigation concerning such terms may be in showing concrete injury to the consumer, often a requirement for standing in court and in the application of certain UDAP statutes. See generally NCLC’s Unfair and Deceptive Acts and Practices § 11.4.2. A case seeking injunctive or declaratory relief may be more viable. Certainly, a state attorney general can challenge contracts containing such terms under the state UDAP statute.

Unfair or Deceptive Practices Involved with Digital Shopping for Financial Products

The CFPB has issued CFPB Circular 2024-01 concerning abusive practices by digital intermediaries that aid consumers who shop online for financial products. These intermediaries include websites, applications, or chatbots that operate as comparison-shopping tools, which consumers turn to for help with researching, comparing, and selecting consumer financial products or services. It also includes lead generators that collect data directly from consumers by advertising websites that present themselves as helping consumers get a loan or connect with lenders.

Such digital intermediaries often receive remuneration or other benefits, sometimes referred to as “bounties” by market participants. The CFPB finds that these companies engage in abusive practices when they steer consumers to certain products or services based on remuneration to the operator, not based on the best interest of the consumer.

While the circular focuses on these practices as violations of the CFPB abusive standard, the same practice may be considered unconscionable, unfair, or deceptive, if for no other reason than it violates federal law (i.e., the CFPB abusive standard). Abusive and unconscionable are similar standards and the same can be said for the unfairness standard, although the consumer might also have to show the practice does not significantly benefit competition.

Protections for Corporate Whistleblowers

CFPB Circular 2024-04 indicates that employees of financial services companies should be protected if they disclose violations of federal consumer financial laws to government investigators. Employment contracts cannot have terms that could lead an employee to reasonably believe that they would be sued or subject to other adverse actions if they disclosed such information. See 12 U.S.C. § 5567.

While the circular focuses on terms that discourage cooperation with government agencies, such terms in employment contracts being contrary to law should be unenforceable even where the employee provides information to private litigants.

Standards for Home Appraisals

The CFPB, OCC, FRB, FDIC, NCUA, and FHFA have adopted a final rule, effective not until October 1, 2025, to implement the quality control standards mandated for the use of automated valuation models (AVMs) by mortgage originators and secondary market issuers in determining the collateral worth of a mortgage secured by a consumer’s principal dwelling. See 89 Fed. Reg. 64,538 (Aug. 7, 2024).

Driven in part by advances in database and modeling technology and the availability of larger property datasets, the mortgage industry has begun to use AVMs with increasing frequency as part of the real estate valuation process, and the concern is the accuracy of those systems and whether they violate nondiscrimination laws. Under the final rule, institutions that engage in certain credit decisions or securitization determinations must: adopt policies, practices, procedures, and control systems to ensure that AVMs used in these transactions to determine the value of mortgage collateral adhere to quality control standards designed to ensure a high level of confidence in the estimates produced by AVMs; protect against the manipulation of data; seek to avoid conflicts of interest; require random sample testing and reviews; and comply with applicable nondiscrimination laws.

For more on federal law regarding mortgage appraisals, see NCLC’s Mortgage Lending § 7.6.

Related Publications

{kind=link}

Free First Chapters

The first chapter of each consumer law treatise is available for free in NCLC's Digital Library.

Click any NCLC title below to start reading now:

Debtor Rights

Fair Debt Collection

Consumer Bankruptcy Law and Practice

Student Loan Law

Repossessions

Access to Utility Service

Mortgages & Foreclosures

Mortgage Lending

Mortgage Servicing and Loan Modifications

Home Foreclosures

Deception & Warranties

Unfair and Deceptive Acts and Practices

Federal Deception Law

Automobile Fraud

Consumer Warranty Law

Credit & Banking

Fair Credit Reporting

Truth in Lending

Consumer Credit Regulation

Credit Discrimination

Consumer Banking and Payments Law

Consumer Litigation

Collection Actions

Consumer Class Actions

Consumer Arbitration Agreements